The first step in personal financial planning is controlling your day-to-day financial affairs to enable you to do the things that bring you satisfaction and enjoyment. This is achieved by planning and following a budget, as discussed in the first article in this series.

The second step in personal financial planning, and the topic of this article, is choosing and following a course toward long-term financial goals. As with anything else in life, without financial goals and specific plans for meeting them, we drift along and leave our future to chance. A wise man once said: "most people don't plan to fail; they just fail to plan." The end result is the same: failure to reach financial independence.

The third step in personal financial planning, "Building a Financial Safety Net," is discussed in the third article in this series.

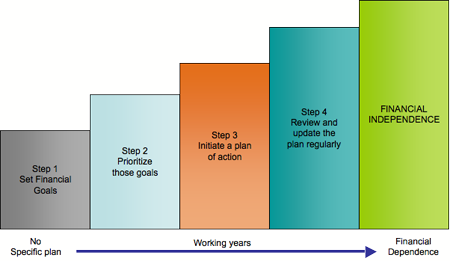

FOUR SIMPLE STEPS FOR SETTING FINANCIAL GOALS

Step 1: Identify and write down your financial goals, whether they are saving to send your kids to college, buying a new car, saving for a down payment on a house, going on vacation, paying off credit card debt, or planning for retirement.

Step 2: Break each financial goal down into several short-term (less than 1 year), medium-term (1 to 3 years) and long-term (5 years or more) goals.

Step 3: Educate yourself! Read Money magazine, or a book about investing, or surf the Internet's investing web sites. The stock market is not voodoo. With a little effort you can learn enough to make educated decisions that will increase your net worth many times over. Then identify small, measurable steps you can take to achieve these goals, and put this action plan to work.

Step 4: Evaluate your progress. Review your progress monthly, quarterly, or at any other interval you feel comfortable with, but at least semi-annually, to determine if your program is working. If you're not making satisfactory progress on a particular goal, re-evaluate your approach and make changes as necessary.

DO IT NOW!

There are no hard and fast rules for implementing a financial plan. The important thing is to do SOMETHING, and to start NOW.

First Step to Financial Success

Personal financial planning consists of three general activities:

- Controlling your day-to-day finances to enable you to do the things that bring you satisfaction and enjoyment.

- Choosing and following a course toward long-term financial goals such as buying a house, sending your kids to college, or retiring comfortably.

- Building a financial safety net to prevent financial disasters caused by catastrophic illnesses or other personal tragedies.

This article addresses how to achieve the first of these goals: controlling your day-to-day financial affairs. See "More of This Article Series" in the box to the top right for Step Two: "Setting Financial Goals," and Step Three: "Building a Financial Safety Net."

Why Should I Budget?

Controlling your financial affairs requires a budget. For many people, the word "budget" has a negative connotation. Instead of thinking of a budget as financial handcuffs, think of it as a means to achieve financial success.

Whether you make thousands of dollars a year or hundreds of thousands of dollars a year, a budget is the first and most important step you can take towards putting your money to work for you instead of being controlled by it and forever falling short of your financial goals.

To those of you who think you know where your money goes without keeping detailed records, I issue this challenge: keep track of every cent you spend for one month. I promise you'll be surprised and perhaps shocked by how much some of your "small" expenditures add up to.

For an eye-opening illustration, try the American Express Saving or Spending Big Calculator. Enter the cost and frequency of a habit or indulgence and how many years you expect it to continue. Click a button and see not only how much you'll spend over the specified time period, but how much that same amount would grow to if you invested it at various rates of return. Mind-boggling!

Budgeting and tracking your expenses gives you a strong sense of where your money goes and can help you reach your financial goals, whether they are saving for a down payment on a house, starting a college fund for your kids, buying a new car, planning for retirement, paying off the credit cards, or saving for that trip to Aruba.

Since financial matters are one of the leading causes of marital discord and divorce, getting a handle on your spending, implementing a budget, and saving for the future can also have positive effects on your relationship with your spouse or partner.

Should I Use a Software Program?

You don't need to invest in fancy software in order to do a budget, but a good software program WILL make the job easier, and being able to print out graphs and reports from your PC can serve as a motivation for entering all that data.

Many banks are now offering free PC banking and free personal finance software. You simply dial into the bank's computer (or your bank may use web-based banking), and download the checks that have cleared your account, directly into your personal finance software. Then you indicate an expense category for each check.

You can do a basic comparison of budget versus actual expenses by category, or you can enter more detailed information such as investments, assets, liabilities, etc., and print personal financial statements showing your net income and net worth.

Some of the most popular personal finance software programs for checkbook and expense tracking are: Quicken, MS Money, and MoneyDance.

Whether you use sophisticated personal finance software or a couple of pieces of paper and a pencil, the important thing is that you get on the road to financial freedom by starting a budget today.

The $ Adds Up...

| Habit | Yearly Cost |

| Daily Cup of Coffee | $547/yr |

| 2 Packs of Cigarettes/Day | $2555 - $3285/yr |

| 1 Hardback & 3 Paperback Books/Mo. | $690/yr |

| Lunch Take-out 5 days/wk @ $5-$10/day | $1300 - $2600/yr |

| 3 Drinks at a Bar/Wk. | $936 - $1092/yr |

| 3 Six-packs of Coke/Wk. | $624 - $936/yr |

Syed Rory

BANDAR SERI BEGAWAN

Wednesday, April 2, 2008

A TOTAL of 120 officers from the Employees Trust Fund (TAP) on Monday brushed up on their financial know-how as part of a month-long roadshow aimed at enhancing their financial planning prowess.

The roadshow was also a refresher course for senior employees which will be held annually once a year.

Throughout April, TAP will organise the roadshow for selected institutions such as BRUNEI Shell Petroleum Company, Brunei Liquified Natural Gas, Brunei Gas Carriers Sendirian Berhad, Universiti Brunei Darussalam, Institut Teknologi Brunei and Royal Brunei Armed Forces as part of activities to commemorate the 15 years establishment of TAP.

The roadshow will include financial institutions such as Bank Islam Brunei Darussalam, HSBC, Standard Chartered Bank, CIMB and Baiduri Bank for visitors to learn about the financial planning systems that have been implemented by these institutions.

Some of the institutions have also brought in an expert to speak on the subject. A representative from the Brunei Islamic Religious Council will also be on hand to speak about zakat and its significance towards proper financial planning.

A lecturer from CIMB Islamic, Malaysia, Mohd Damshal Damit briefed the 120 TAP employees, while the briefing on zakat was presented by Ustaz Muhammad Shukri Hj Ahmad.

The Brunei Times

Standard Chartered Bank continues to lead the way by introducing value added services for its customers in its efforts to assist customers in making the right decisions when it comes to financial matters.

Customers looking to purchase a new home or to simply upgrade to a larger family home, can now gather useful tips and insights on how to go about beginning the purchase process with Standard Chartered’s Home Ownership Guide.

In this guide book, prospective home owners are guided step by step on managing finances in order to make their home purchase a reality, from documentation required for applying for housing loan to handy tips on house renovation.

“We understand how daunting the whole process of buying your own home can be, especially for first time home buyers where documentation and legal procedures may seem confusing. Hence, Standard Chartered is pleased to offer this extra guide to help home buyers or the interested public to not only make better financial decisions but to give a clearer picture on the process and stages of home purchase. Purchasing one’s own home is a special occasion and does not happen on a regular basis, hence Standard Chartered believes that being the right partner means being able to give dependable advice on what works best for each individual customer”, commented Ms Lim Su Hui, General Manager, SME and Mortgages.

This handy guidebook is available to all at any Standard Chartered Bank branch. Those interested in finding out more about the guidebook or about home loans can contact Standard Chartered’s Phone Banking Centre at 265 8000, or visit any Standard Chartered Bank branch where a Personal Financial Consultant will be on hand to assist.

There is a need for higher contribution rates from employers and employees to supplement the current Employees Trust Fund (TAP) in the country, as its current contribution rates are too low by regional standards.

This was one of the points made during the Social Security Roundtable 2008, themed "Towards A More Sustainable Post-Retirement Income, Policy Options For Brunei Darussalam", organised by the Centre for Strategy and Policy Studies (CSPS) on Saturday at the Empire Hotel and Country Club, Jerudong.

Earlier, Permanent Secretary at the Prime Minister's Office Pengiran Dato Paduka Haji Ismail bin Haji Mohamed in his capacity as CSPS Chairman, in his opening address, said the locals have been blessed with a decent quality of life and standard of living, but the sustainability of these components require the analysis of a number of key variables.

He noted one of which is TAP's contribution rate of five per cent, by both employers and employees, is too low to fund accumulated savings upon retirement.

"Currently, the normal pension age is 55, and it is estimated that there are more than 20,000 people in the age group of 55 and above," said the permanent secretary. "With current demographic data, the aging population in 20 years time will increase considerably, coupled with longer life expectancy."

Therefore, he said, "the increased number of 'warga emas' need to have certain level of income in order to support their way of life".

Pengiran Dato Paduka Haji Ismail, in his welcoming remarks, also emphasised on CSPS's commitment to advanced research and analysis on topics that are of strategic importance to the country's interest.

A report, finalised by CSPS, shows clear indication that the current pension schemes, particularly during post-TAP era, are far from adequate if there are no other provisions of savings, he said.

As such, Saturday's dialogue was aimed at discussing alternatives and required improvements to existing social security options in the country, particularly with the view of improving the Post Retirement 'Safety Net' and Financial Security for post-TAP participants.

In conclusion, there is a need for higher TAP contribution rates, and such schemes should not allow for withdrawals, in order to provide an income stream in retirement.

It was also noted that given the sluggish business conditions, the capacity for private sector to participate in increased contributions may be limited.

Among the other issues discussed during the roundtable was the importance of education in instilling a culture of savings and self-reliance.

Meanwhile, the dialogue, moderated by CSPS board member Stephen Ong, brought together over 100 stakeholders, policymakers, members of both public and private sectors, together with panellists from the World Bank, American International Group (AIG), Singapore Ministry of Manpower, and TAP.

The findings and recommendations from two independent research teams, represented by World Bank's Mark Dorfman and AIG Global Investment Group Vice President Michael Hudnall, were shared and discussed during the roundtable.

The event also saw a presentation by Deputy Permanent Secretary at Singapore Ministry of Manpower Aubeck Kam, who shared Singapore's workforce concept and touched on some social security schemes in Singapore.

Following the roundtable, CSPS will make available a report, with observations from the roundtable, to relevant authorities for policy considerations.

Most people spend first... and try to save and invest what little is left

Why can't we save money?

The answer is within yourself. Identify your weakness. Some of the reasons could be:

- Poor earning capabilities

- Too many debts - credit card, loan installments: personal, car, computer, furniture etc

- Excessive spending

- Luxury items, over-budget (no budget at all) e.g. must have latest mobile phones, laptops etc

- Frequent holiday trips

Blogged with Flock